By Steve Brian, March 31, 2022

Grab yourself a cup of something that makes you happy, find a cozy nook to sit in, and let’s talk about appraisals for a minute…

Appraisals, appraisals, appraisals – they are my least favorite aspect of the transaction since they are something I have only the tiniest (translation: almost no) amount of control over, which I’ll get to down below. With prices continuing to trend upward and offers going so high over list price, one of the terms in offers that has become a key aspect to having your offer accepted is being able to offer an “appraisal buffer” to the Seller.

“Steve, what’s an appraisal buffer?”

Good question, I’m glad you asked. While the language from agent to agent varies, it is usually written out along the lines of, “In the event of a low appraisal, Buyer agrees to bring up to $__,___ to the transaction to allow the sale to proceed to close.” You can also waive your appraisal contingency altogether, but you do need to have the cash available to make sure you can back that up without the risk of losing your earnest money. This all depends on how much cash you have available, what your comfort level is, and how much you want the house. There’s no one-size-fits-all approach to this discussion, so I’m giving it my best shot and am happy to chat further if you have any questions about the information presented below.

So…how exactly does this play out when/if the appraisal DOES come in low? Well, let’s assume you see a house listed for $500k and YOU. WANT. IT. One of the terms, among many, that we will be going over is the appraisal buffer. I’ll start off by running comps which, in this market, are not helpful in determining a winning price, but are helpful in giving you an idea of what I *think* the appraisal will come back in at. Again, I have no control over what the appraiser’s final opinion of value will be, but this step helps you make a decision on what you’re comfortable with based on the market data available to us at the time you write the offer.

Circling back to the tiny amount of control I do have with appraisals, here is what I will do once we’re in contract and getting close to the appraisal appointment…

Run the most current comps the day before the appraiser goes out to the house.

Run market trends to account for appreciation and apply that year-over-year growth to all of the comps I plan to send to the appraiser.

Talk to the listing agents all of the pending sales nearby and see if any of them are willing to share the price/terms under which they are currently pending.

Appraisers don’t always factor in pending comps, but if there’s even a chance, I’m gonna take a shot for my clients!

Look at all aspects of the market data and put together a “Supporting Information for the Appraisal” email to send over to the appraiser.

This email is sent with respect for the appraiser and their own process. Keeping up with rising prices is hard for appraisers and they’re doing the best they can. I’m just trying to help make their job a little easier if possible 🙂

With that in mind, let’s get back to writing the offer…

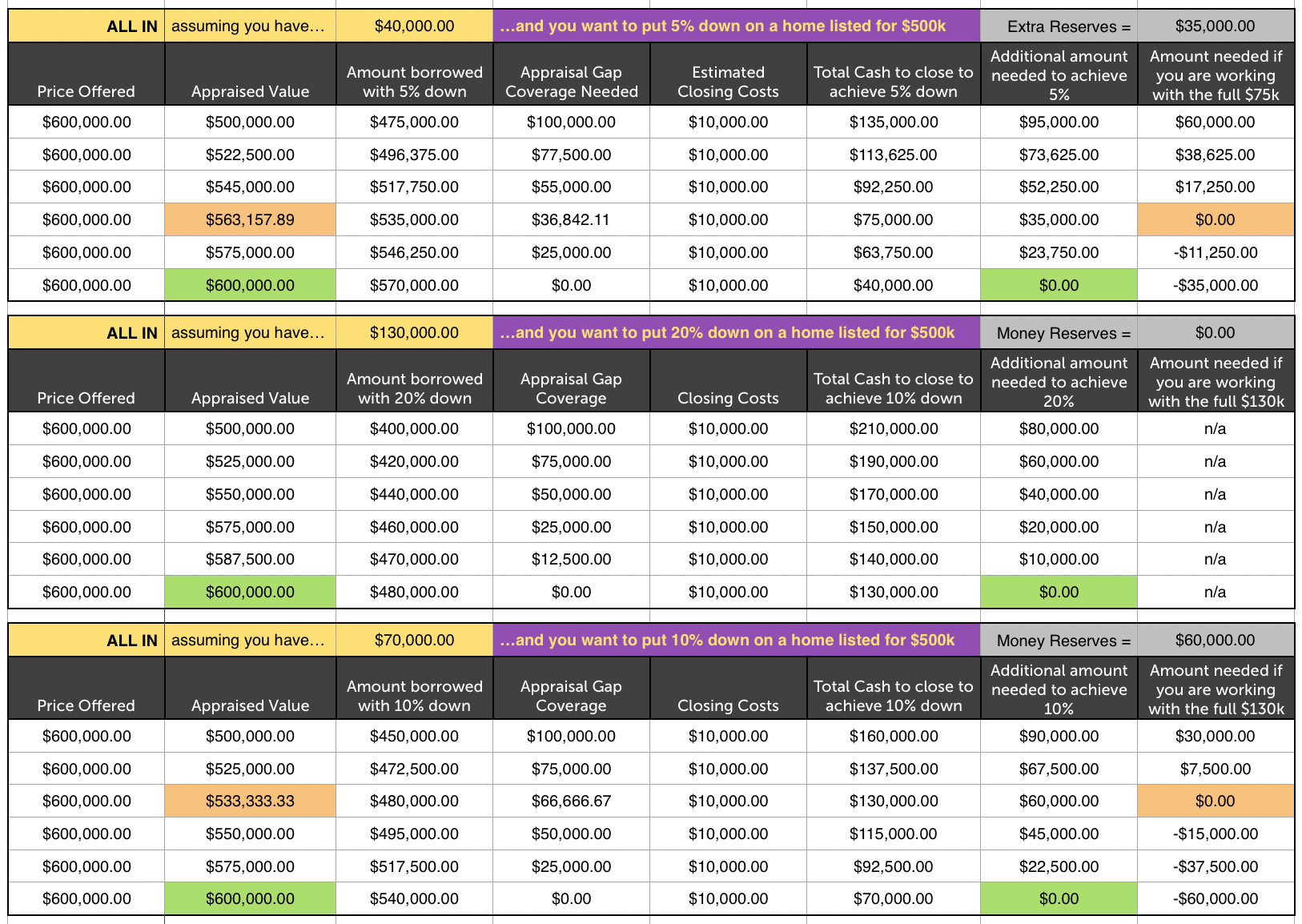

Assuming (a) the house is listed at $500, (b) the comps seem to indicate a potential value of $535, and (c) you want to offer $600k, you’ll need to be ready to make up that extra $65k in the event of a low appraisal. For the spreadsheet below, let’s assume two scenarios, both of which assume closing costs (which are separate from the down payment) are $10,000…

SCENARIO ONE

You have 5% down plus the $10k for closing costs and an extra $35k to play with.

This is showcased in the first section of the spreadsheet.

SCENARIO TWO

You have $130,000, which covers 20% down plus the $10k of closing costs.

This is showcased in the second two sections of the spreadsheet.

Now, without further ado, below is a spreadsheet of the different scenarios outlined above, along with a very short explanation below the graph.

Short Explanations:

- With the 5% down scenario, you’d need the appraisal to come in with a value of ~$563,000 for the seller to get the $600k you’ve offered.

- To achieve 20%, you’d need the value of the appraisal to come in at $600,000, but if it comes in less than that, you could still put down 10% (or more) if the value of the appraisal comes in at least ~$533,350

If you want to know exactly how all of this will affect your monthly payments, you’ll need to speak with a qualified lender. If you don’t already have one you trust, I couldn’t recommend a lender more highly than Pat Lindgren @ Do Good Mortgage: 503-713-7863 / pat@dogoodmortgage.com

This is all a lot to take in through a blog format, so please do reach out to me if you have any questions at all about the appraisal info I’ve covered and/or the overall home-buying process in today’s market! My goal is to provide you as much information as possible so that whatever decision you end up making is a well-informed one!

Steve Brian

Broker | OR

He/Him

Steve has made his career based on the concept that “service comes first.”

He has helped clients buy and sell homes on both sides of the river and has a strong understanding of what it takes to negotiate in a way that allows his clients to feel that their best interests are always at the forefront of the negotiation table. He has worked with first time buyers, upsizers, downsizers and investors alike, priding himself on being able to provide well-informed advice based on the current market and leaving the final decisions up to his clients!

After moving to Portland in 2002, Steve bounced around different neighborhoods on the Eastside of Portland and grew a love for straight shots of espresso. He has now planted roots with his family in the Terra Linda neighborhood of NW Portland and is a sucker for a delicious beer on a hot, summer day from one of the many local breweries in Portland. When he’s not wearing his “Steve the REALTOR®” hat, he likes to spend time in the water with his two boys or just put on some mud boots and find some trails to explore.

"Service Comes First!"

Read More

- T: 503-720-2529

- steve@stevebrian.com