By Jon Gould-Knight, February 21, 2025

TL;DR

- Waiting for rates to drop might not save you money if home prices keep rising.

- First-time buyers may still build more wealth by buying now instead of waiting.

- If you already own a home with a lower interest rate, the decision to move is about more than just the mortgage—convenience, lifestyle, and equity should all be considered.

- You may have more equity than you think, and rolling it into a new home could make moving more feasible than it seems, even with a higher rate.

Don’t Wait for Mortgage Rates to Drop—Here’s Why

I hear people say all the time, “I’m going to wait until mortgage rates go down before I buy my next home.” That makes sense in theory—after all, a lower interest rate means a lower monthly payment, right?

But here’s the thing: waiting for rates to drop doesn’t guarantee savings. Home prices tend to rise over time, and interest rates may not fall as quickly as many hope. The longer you wait, the more you may end up paying—either in appreciation, in lost equity-building opportunities, or in the emotional and practical costs of staying in a home that no longer fits your needs.

What If This Is Your First Home?

If you’re a first-time buyer, you might be thinking:

“If I wait, I can get a lower mortgage rate and a lower monthly payment.”

It sounds logical, but let’s look at the bigger picture.

A $350,000 home bought today at a 6.8% interest rate will cost more per month than the same home at a 6.25% rate in a year or two—but will that home still be $350,000 by then? If it appreciates even 5% per year, that home could cost $375,000 or more in the near future, wiping out the benefit of a slightly lower rate.

Meanwhile, during the time you wait, you’re still paying rent, which builds zero equity for you. Buying now means you start paying down a mortgage immediately while also benefiting from home appreciation.

A Quick Example:

- Buying Now: A $350,000 home with 10% down at a 6.8% rate → $2,150/month principal + PMI & interest

- Buying Later: A $375,000 home with 10% down at a 6.25% rate → $2,250/month principal + PMI & interest

You may save $1,200 your first year, but you have missed out on that $50,000 in equity that your house gained just by existing! And that’s before considering that rent prices tend to rise over time, too.

What If You Already Own a Home with a Lower Interest Rate?

A lot of homeowners are sitting on interest rates below 4% from when rates were at historic lows. The thought of giving that up to buy a new home at today’s 6-7% rates is, understandably, hard to accept.

But the question is: Is staying in your current home actually the best financial AND lifestyle decision for you?

When the Numbers Aren’t the Only Thing That Matters

I talk to a lot of homeowners who feel stuck—they don’t want to give up their low mortgage rate, but they also feel like their current home isn’t working for them anymore..

- Cramming into too little space? That extra bedroom or larger kitchen could dramatically improve your day-to-day life.

- Tired of the layout or neighborhood? Sometimes, your priorities change, and your home no longer suits them.

- Wishing for a shorter commute? A little extra in your monthly payment could be worth the time saved each day.

Money is important, but so is your comfort, happiness, and time.

Your Home Equity Might Be the Key

If you’ve owned your home for several years, you may have more equity than you think. The average homeowner gained over $30,000 in equity in 2023 alone—and in some markets, even more. That equity can be rolled into a new home, reducing your loan amount and making the higher rate less of a burden.

For example:

- You bought a home for $350,000 five years ago with 10% down.

- It could now be worth $480,000 now

- Let’s say you still owe $295,000 on your mortgage.

- That’s $180,000 in equity that you could use toward a new purchase.

Even if you buy a more expensive home, your large down payment helps keep the new mortgage manageable—offsetting some of the pain of today’s higher rates.

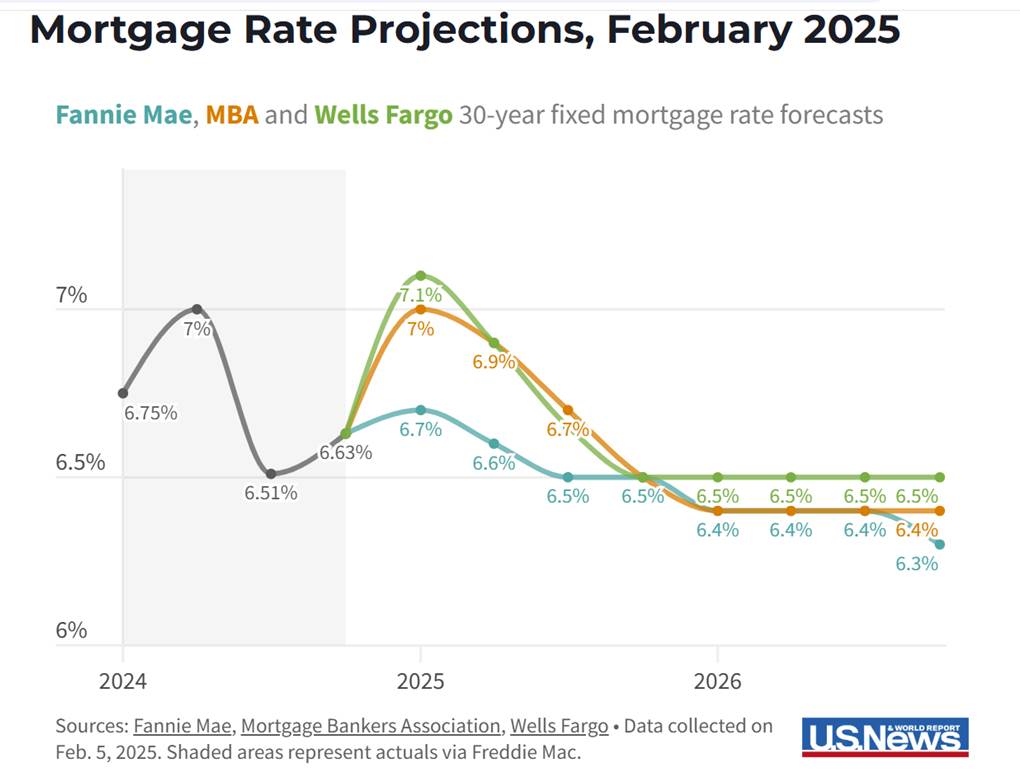

Will Mortgage Rates Drop Anytime Soon?

Nobody has a crystal ball, but most projections suggest mortgage rates will stay above 6% for the foreseeable future. Even if they do drop, it’s likely to be a gradual decline, not an overnight plunge.

And here’s the thing: If rates do drop significantly in the future, you can always refinance. But waiting to buy a home that fits your life right now could cost you in rising home prices, lost equity opportunities, and the personal costs of staying in a home that no longer works for you.

The Bottom Line

Waiting for lower rates might seem like a safe strategy, but in many cases, it costs more than it saves. Whether you’re a first-time buyer or a current homeowner, focusing only on interest rates can cause you to overlook other key factors—like appreciation, equity, and quality of life.

The right time to buy isn’t just about the rate. It’s about your financial situation, your lifestyle needs, and your long-term goals. If you’re unsure what makes sense for you, let’s talk. The best decision is an informed one.

Jon Gould-Knight

Broker | OR & WA

He/Him

Hello! I’m a heart-centered real estate agent based in Vancouver, serving folks throughout Southwest Washington. My goal is to help you find more than just a house—I want to help you find a home that truly feels like yours...

Read More

- T: 360-995-8551

- jon@cominghomepnw.com