Find out what’s happening in the Portland real estate market for Early-June 2023.

Hi! I’m Atika Hagen, Broker with Living Room Realty here to tell you what you need to know about the market for early June 2023.

You may remember me from the last market update where Jenelle started singing, “It takes two to make a thing go right.” Well I’m here to tell you that that’s still true. Entering into the summer months, the market has been known to slow down, but we in Portland are actually seeing the opposite.

Pricing

The median price for a home in Portland right now is $699,000, this is the highest we’ve seen since the peak during the nutso market in the throes of the pandemic. At its peak – it’s peak!- in February of 2021, the median house price was only $950 more than right now, clocking in at $699,950.

Market Action

In our office, which holds the number one market share in Portland, we’ve seen fifty deals close in just the last two weeks alone. As well, inventory has increased by 42% from April to now. We’ve also seen the number of days on market for homes steadily decrease since March, from 102 days to currently sitting at 75 days. This tells me that unlike my children, the housing market in Portland will not be taking a summer vacation.

But what does all this mean in terms of real world examples for someone currently buying or selling?

Get Creative

Well as the market has begun to warm, I’ve had a few clients forgo sought after neighborhoods for other homes that are clean, landscaped, staged well and have creative touches. What this is showing me is that if you do those extra things to make your property stand out, it can go a really long way.

In another instance a client had an offer accepted under list price, but to pull that off we had to get creative with terms. As a buyer it’s important to know that it’s not always about the dollar amount. Having a knowledgeable realtor by your side that can think outside the box is crucial.

Living Room Realty is committed to connecting you with as much information to help you make an informed decision. If you’re ready to make a move, give me a call today. I’d love to help you find your next Living Room.

If you find the current Portland real estate market overwhelming, you’re not alone. The good news is, new spring listings are popping up every day! Just not as many homes are available as there are buyers for them. Inventory is low and that creates a lot of organic competition, especially for the “best” properties. Homes that have been freshly remodeled, have a lot of style, and/or are in prime locations command attention, premium prices and aggressive terms. Many buyers feel priced-out after being out-bid in multiple-offer situations. Avoid Buyer’s Burn-out!

It can be hair raising!

Fortunately, we’ve been at this a long time, and have assisted clients through every possible market on the spectrum.

Tips for nabbing your next home using creative shopping strategies:

I am not kidding about this- visit homes with ugly pictures! Beyond all the clutter and poor lighting you may find your treasure, hidden in plain sight and overlooked by most.

Consider properties that are showing a bit of wear and take on the project yourself to make it really shine. Sweat equity is real, but be honest with yourself. What resources will you have available to spruce up your new place. Is watching a how-to YouTube enough to help you handle the fixes, or will you need to hire experts? Skip wonky staircases, wacky floor plans and locations near freeways, bus stops, and busy streets. Buy smart!

Look at homes priced well below your budget to give you room to fight and be the winning bidder!

Shop slightly above your current price range. Consider properties that have been on the market a while (translation: homes that are likely over-priced).

Explore less expensive locations.

Re-evaluate your priorities and consider smaller homes and yards, homes without recent updates, etc.

How we can help!

Bonnie Roseman and Trish Sunderland, Dynamic Real Estate Duo in Portland, OR

There are a few things we are doing behind the scenes for our buyer clients to help get them to the finish line. We scour Coming-Soon listings on the regular. We hustle to get our buyers into homes as soon as they hit the market. Pro tip: It’s not unheard of to persuade a seller to accept a compelling offer on day one on the market, thus avoiding a bidding war. We review old and expired listings and contact off-market homeowners who might consider selling. We leave no stone unturned to help you find your next home!

What can you do?

Get organized and prepare yourself. Consider your financing options and make a decision early in your journey. Where you will obtain your new mortgage? Your lender is your partner, just like your Realtor, in the homebuying process, so make sure you choose trusted advisors! Submit all of the needed documents and ask your lender to run your file through underwriting. Keep in touch with them and make sure you are crunching numbers using current interest rates and realistic estimates for property taxes and homeowner’s insurance. Don’t fall in love with a home only to discover the cash you need to close the deal, or to carry the monthly payments, are beyond your comfort level –OUCH!

If you have the good fortune to be paying with cash, make sure you have proof of funds at the ready!

Financial readiness means your documentation is ready to go!

If you are a cash buyer, or have a large down payment, have proof that the funds required for your purchase are in a checking or savings account in your own name. Believe it or not, mutual funds, ETFs, gifts and the like are NOT considered cash!

Engage a lender early, then obtain an up to date mortgage pre-approval letter that reflects the current interest rate and the property tax amount for each specific property you are considering. Your lender will also help you crunch the numbers so you know you are comfortable with the amount of cash you will need to close your purchase and cover the monthly carrying costs. If you love your lender- wonderful! If you don’t have one picked out yet, have no fear, we can connect you with a personal referral to a top notch local pro.

On your mark

Drive, bike or walk by exciting new listings the first day on the market. Let your Realtor know right away when a place shows possibility and make yourself available ASAP to get inside. After all that hurrying, be prepared to wait patiently. Many of the most desirable properties will have due dates for offers a while out and you will need to bide your time.

Understand pricing

Be prepared for newly-listed homes to sell for significantly more than the asking price, sometimes by a wide margin. If the listing has been on the market for 10-20 days it will probably go for right around asking price, and if it has been sitting for more than a month without a recent price reduction, a bigger discount may be in the cards.

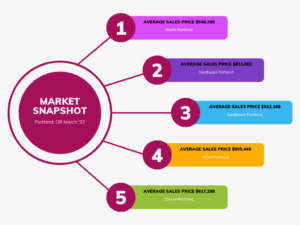

You can stay up-to-date with current market conditions with the weekly Portland report from Altos Research.

Average sales price in Portland, OR

Offer Terms- Price is not the only thing that matters to home sellers. Sometimes having the best terms can keep you in the running, or at least get you the opportunity to modify your offer without it being rejected out of hand, even if your offer isn’t the highest bid. Consider including terms that give the seller confidence in choosing you as their buyer.

When we work with our buyer clients, we discuss many creative ways to strengthen an offer. Two of the key items that can often make a difference are:

Repairs

When it comes to repairs, sellers want to know that they will not be nickel-and-dimed during the inspection process. While most buyers are not in a position to make totally as-is offers, it IS possible to limit the risk to the seller without leaving yourself wide open. One strategy is to commit to accepting responsibility for needed repairs that fall below a certain threshold. This way the seller knows you will only attempt to negotiate if something big comes up.

Appraisals

As prices increase, it can become very challenging for appraisers to find past home sales (AKA “comps”) that keep up with current values. This does not mean the value is not there, but rather that the data is not keeping up with rapid increases in market values. When a home appraises for less than the contract price, this is known as an “appraisal gap” because lenders base financing on the appraised value, not the purchase price.

Sellers want to know that you will close the transaction, even if there is an appraisal gap. You can solve this by adding cash to your down payment. Another approach is to keep your loan amount and down payment as planned, but preparing yourself for an adjustment in the Loan-to-Value ratio. This may have a small impact on your monthly payments in some cases. In others, it may have no impact on you at all!

Here’s an example:

If you are paying $100,000 for a home, putting down $8,000 and borrowing $92,000 (92% Loan-to-Value), but your appraisal comes in at $95,000, you could still borrow $92,000 – it would just be underwritten at a higher Loan-to-Value because the LtV is based on the appraised value.

100,000 sales price x 92% = $92,000 loan amount.

95,000 appraised value x 96.8% loan-to-value = $92,000 loan amount

The down payment is $8,000 either way!

Ready, Set, Go!

We pride ourselves on assisting clients to be selective in their home purchase decisions and writing offers with a high chance of acceptance in order to avoid a roller coaster ride. When you or your peeps are ready to buy – or even just thinking about buying in the future – it is always in your best interest to prepare ahead of time, with a solid team in place for when it’s time to make the leap. Drop us a line us at portland@realtor.com to get on our dance card! Thank you for trusting us. Your new home awaits and we WILL get you to the finish line!

Potential homebuyers in Clark County face a difficult decision as the real estate market continues to normalize: Buy now or wait?

The median sale price for residential homes in Clark County continued falling last month, dropping from $514,000 in November to $479,900 in December, according to the most recent Regional Multiple Listing Service report. Interest rates for 30-year fixed mortgages also fell and are now just above 6 percent, according to the government-sponsored home mortgage packager Freddie Mac.

“If they buy now, regardless of what they can afford, it’s always going to be better than renting because rent tends to always go up,” Cotrell said. “If you lock in a mortgage rate, it’s locked in for that life of the loan, and you know how much your expenses are going to be.”

Even as prices and interest rates fall, Cotrell doesn’t foresee housing affordability improving for potential homebuyers in the near future. Mortgage rates, though lower than their peak of 7.08 percent in November, are still high, limiting buying power.

…

Looking at the year ahead, Cotrell predicts interest rates could fall below 5 percent. If that happens, the market would “take off like crazy,” he said.

For this reason, he thinks buying now would be beneficial for those who want to avoid the stress of a hot market.

What, exactly, is the 2023 housing market going to look like? It’s a difficult question to answer. Some may envision 2023 shaping up to follow in the footsteps of the 2008 subprime mortgage crisis with a possible bubble or crash.

The majority of housing predictions, however, don’t believe we’re in for a huge housing disaster. GOBankingRates spoke to real estate professionals for their take on what’s to come with the 2023 housing market. Here’s what they predict could happen next.

Interest Rates Could Reach 9%

Interest rates will rise as we fight back inflation, said Melissa Dorman, broker at Living Room Realty. Historically speaking, Dorman said a 9% interest rate is not out of the realm of possibility in the 2023 housing market.

If you feel nervous at the thought of 9% interest, try not to panic. There’s not an expectation that homes will sell at outrageous percentages, like 25% over the list price, anymore, said Kim Parmon, principal broker at Living Room Realty.

“If rates continue to rise in earnest I expect we will see both low supply and lower demand, which will likely create a relatively flat market,” Parmon said.

Interest rates, Dorman predicts, are anticipated to come down once we enter a recession. Buyers brave enough to buy now will be able to refinance their homes at a lower interest rate. As interest rates fall, likely in 2023, buyers will return to the market again.

Buyers Remain Cautious but Fortune Favors the Bold

Based on birth rates, a steady influx of new buyers in their early 30s will be in the housing market each year. Despite these birth rates, Parmon said buyer demand is down. The interest rates have risen and as a result, buyers are not rushing to purchase homes.

Buyers Remain Cautious but Fortune Favors the Bold

Based on birth rates, a steady influx of new buyers in their early 30s will be in the housing market each year. Despite these birth rates, Parmon said buyer demand is down. The interest rates have risen and as a result, buyers are not rushing to purchase homes.

What, exactly, is the 2023 housing market going to look like? It’s a difficult question to answer. Some may envision 2023 shaping up to follow in the footsteps of the 2008 subprime mortgage crisis with a possible bubble or crash. GOBankingRates spoke to real estate professionals for their take on what’s to come with the 2023 housing market. Here’s what they predict could happen next.

Interest Rates Could Reach 9%

Interest rates will rise as we fight back inflation, said Melissa Dorman, broker at Living Room Realty. Historically speaking, Dorman said a 9% interest rate is not out of the realm of possibility in the 2023 housing market.

If you feel nervous at the thought of 9% interest, try not to panic. There’s not an expectation that homes will sell at outrageous percentages, like 25% over the list price, anymore, said Kim Parmon, principal broker at Living Room Realty.

“If rates continue to rise in earnest I expect we will see both low supply and lower demand, which will likely create a relatively flat market,” Parmon said.

Interest rates, Dorman predicts, are anticipated to come down once we enter a recession. Buyers brave enough to buy now will be able to refinance their homes at a lower interest rate. As interest rates fall, likely in 2023, buyers will return to the market again.

Buyers Remain Cautious but Fortune Favors the Bold

Based on birth rates, a steady influx of new buyers in their early 30s will be in the housing market each year. Despite these birth rates, Parmon said buyer demand is down. The interest rates have risen and as a result, buyers are not rushing to purchase homes.

“I am seeing buyers be extremely cautious as they navigate purchasing right now. They are fearful that prices may come down in the future,” Parmon said. “Some buyers are choosing to sit out and watch the market and see what happens moving forward.”

However, it isn’t always possible to time any market. When Parmon has seen previous buyer behavior like this, the result has been buyers watch until they realize prices haven’t dipped. Then everyone enters the market at the same time again, creating more bidding wars and price increases with the existing low inventory.

Buyers may certainly be cautious about making a purchase, but some may not be content to sit on the sidelines for another year. The adage “fortune favors the bold” could be the new mantra for those brave enough to buy.

As mentioned earlier, interest rates are anticipated to come down once we enter a recession and allow buyers to refinance at a lower rate. If you’re brave enough to buy now, Dorman said buyers will benefit from a greater inventory, less competition and the ability to negotiate repairs with sellers.

“I think it is a good time to be a buyer. Sellers are having to make more concessions to find the right buyer. There is a larger inventory of homes available,” Dorman said. “The trade-off is the high interest rate.”

Strong Spring 2023 Market Ahead

Parmon, who is based out of Portland, Oregon, predicts buyers will wake up as early as Jan. 2, 2023, and decide to go home shopping. Generally, Parmon said she sees multiple offer scenarios earlier in the year. This levels out approaching the summer months when inventory increases.

Dorman also agrees early 2023 is likely to see a stronger spring market than the fall market. Prices may stagnant or fall in some markets, but the shifts should be nothing like what we have seen in the late spring and early summer of 2022.

“I think the market will balance out and have a slow ramp up as interest rates lower in late 2023 or even early 2024,” Dorman said. “Of course this is all a prediction and I don’t have a crystal ball to foresee the future. This is simply an educated guess based on what I see in the market today.”